The Story of a New Generation

Picture this: You are 24, just out of university, and need a laptop to start your freelance career — priced at VND 20 million. You can comfortably pay VND 4 million per month, but not the full amount upfront. You do not want to go through the paperwork of a bank loan, you feel uncomfortable asking family for money, and traditional credit cards carry interest rates that do not make sense for your situation.

The solution? → BNPL — Buy Now, Pay Later

This is precisely what millions of young Vietnamese consumers need — and exactly why BNPL is the most powerful fintech wave of 2025–2026.

What Is BNPL? How Does the Technology Work?

BNPL (Buy Now, Pay Later) is a short-term consumer credit product that allows buyers to:

- ✅ Receive the product or service immediately

- ✅ Split payment into flexible installments (typically 3, 6, or 12 months)

- ✅ Get approved within minutes via AI-powered decisioning

- ✅ No collateral or extensive credit history required

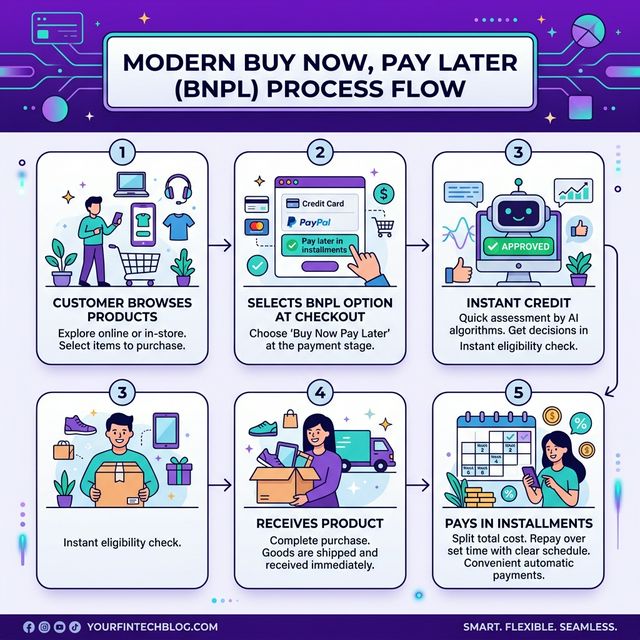

The BNPL Flow: End-to-End

A seamless 5-step journey from product selection to installment completion

Step 1: Customer selects product online or in-store

Step 2: Chooses BNPL as payment method at checkout

Step 3: AI engine analyzes and approves credit in 30 seconds to 3 minutes

Step 4: Customer receives product immediately

Step 5: Automated installment deductions begin on the agreed schedule

P2P Lending: Financial Infrastructure Built by the People, for the People

While BNPL serves consumers, P2P Lending (Peer-to-Peer Lending) creates a direct marketplace between:

- 🏠 Borrowers: Individuals and small businesses seeking capital

- 💰 Lenders: Individuals with idle capital seeking yield above savings rates

The P2P platform acts as a technology intermediary — not a financial intermediary — enabling:

| Benefit for Borrowers | Benefit for Lenders |

|---|---|

| Lower interest rates vs traditional banks | Higher returns vs savings deposits |

| Streamlined digital application process | Diversified investment portfolio |

| No large collateral requirements | Transparent borrower information |

| Disbursement in 24–48 hours | Automated interest and principal collection |

Why BNPL and P2P Lending Are Exploding in Vietnam

Structural Market Drivers:

1. 23+ million “credit-invisible” consumers

Tens of millions of Vietnamese adults have no formal credit history and cannot qualify for traditional bank financing. BNPL and P2P markets create an entirely new credit access pathway — using alternative data rather than legacy credit scores.

2. Millennial and Gen Z consumers dominating spending

Adults aged 18–35 account for over 40% of total consumer spending in Vietnam — and this cohort overwhelmingly prefers digital-first, frictionless financial experiences that avoid branches and paperwork.

3. E-commerce’s exponential growth

Vietnam’s e-commerce market reached USD 25 billion in 2025, with BNPL rapidly becoming the default embedded payment option across major platforms.

4. AI-powered risk modeling outperforms legacy scoring

Rather than relying solely on traditional credit bureau data, modern AI systems can analyze hundreds of behavioral data signals to assess creditworthiness — more accurately and more equitably than legacy models.

FINBLUE: SFIN’s Integrated BNPL & P2P Lending Platform

FINBLUE represents SFIN’s primary product investment in the digital credit space — an integrated platform combining three next-generation financial instruments:

FINBLUE Ecosystem:

┌─────────────────────────────────────────────┐

│ 💳 BNPL Consumer Credit │

│ - Zero-interest installment shopping │

│ - 60-second approval engine │

├─────────────────────────────────────────────┤

│ 🤝 P2P Lending Marketplace │

│ - Direct borrower-lender matching │

│ - Target yield: 8–15% per annum │

├─────────────────────────────────────────────┤

│ 📈 Investment Integration │

│ - Starting from VND 100,000 │

│ - Auto-diversified portfolio allocation │

└─────────────────────────────────────────────┘

Risk Awareness: What Users Need to Know

Responsible fintech means transparent risk communication. Key risks BNPL and P2P users should understand:

⚠️ User-Side Risks:

- Over-leveraging: BNPL’s accessibility can lead to spending beyond capacity if budgets are not tracked

- Late payment penalties: Some platforms impose high fees for missed payment deadlines

- Debt concentration risk: Stacking multiple BNPL obligations simultaneously can create cash flow stress

✅ How SFIN/FINBLUE Mitigates These:

- Automated credit threshold alerts and spending dashboards

- SMS and in-app payment reminders 3 days before due dates

- Transparent credit reporting to help users build verifiable financial histories

- Full compliance with State Bank of Vietnam regulatory requirements

BNPL 2.0: What Comes Next

The next generation of BNPL goes well beyond consumer goods:

- 🏥 Healthcare BNPL: Financing medical bills and dental procedures

- 🎓 Education BNPL: University tuition, professional certification programs

- 🏘️ Housing BNPL: Rental deposits, furniture and home improvement

- ✈️ Travel BNPL: Flights, hotels, and packaged tours

Conclusion

BNPL and P2P lending are not passing trends — they represent a fundamental restructuring of consumer credit infrastructure. For Vietnam, this is a once-in-a-generation opportunity to give millions of people equitable access to financial services while enabling businesses to dramatically expand their addressable market.

SFIN is at the forefront of this shift — not just as a technology provider, but as a genuine partner in building a more financially inclusive Vietnam.

Leave a Reply

You must be logged in to post a comment.